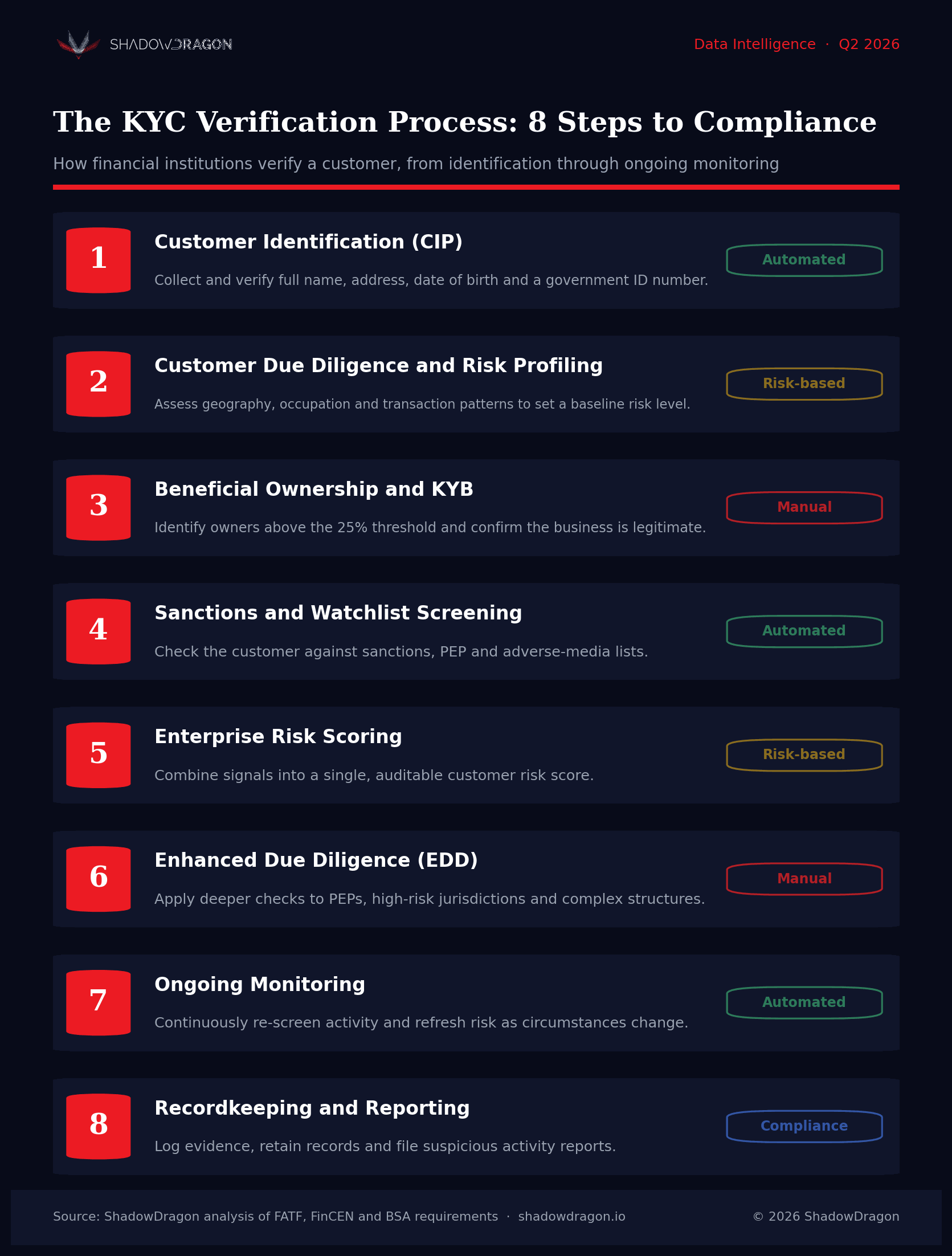

Step 1: Customer identification program (CIP)

A Customer Identification Program is the process of gathering and verifying a customer’s basic identity information before opening an account or commencing a transactional relationship. It forms the first step in KYC document verification and the broader KYC process.

Under CIP, institutions collect KYC identity verification details such as the customer’s full name, residential address, date of birth, and a government-issued identification number (e.g., passport, national ID, driver’s license). These documents are then authenticated, and the information is cross-checked against trusted sources, such as government databases or credit bureaus.

CIP requirements vary based on customer type:

- Individuals must provide personal identification documents and often proof of address.

- Corporate entities must provide business registration certificates, articles of incorporation, tax identification numbers, and details of beneficial owners and controllers. This helps the institution understand the natural persons who own or control the company.

Identity document verification technology, biometric verification, and trusted data sources are used to confirm the authenticity of identity information. These tools are useful for detecting tampered with or invalid ID images, expired licenses, or mismatched records, as well as automating verification checks against official registries or watchlists.

Pair document checks with open-source intelligence corroboration. With ShadowDragon Horizon®, investigators can confirm that names, emails, and addresses show a normal online footprint, spot reused usernames, and flag synthetic profiles with no history.

A robust CIP sets a verified foundation for ongoing due diligence and monitoring.

Step 2: Customer due diligence and risk profiling

Building on the verified identity established in Step 1, institutions proceed with Customer Due Diligence and risk profiling, a comprehensive, risk-based evaluation that both establishes an initial risk rating and supports ongoing, enterprise-level risk management.

Assess the risk profile

CDD begins with relationship-level checks to understand the customer’s potential exposure to money laundering, terrorist financing, or fraud. Analysts review:

- Customer type – individuals vs. corporate entities, and the complexity of their structures

- Geography – countries of residence, operation, or transaction corridors, including FATF high-risk or non-cooperative jurisdictions

- Business/occupation – industries with elevated cash flow or regulatory risk (e.g., casinos, cryptocurrency exchanges)

- Purpose and source of funds – origin of income, intended use of the account, and consistency of stated purpose with expected activity

OSINT enhances this stage by revealing contextual signals that formal documents often miss, such as undisclosed ownership links, extremist views, reputational red flags, or media and community activity consistent with declared business operations. ShadowDragon Horizon® unifies these open-source findings alongside traditional CDD data, giving analysts a more complete picture of the customer’s risk posture before onboarding.

These factors yield an initial risk rating that informs onboarding decisions and determines the frequency of monitoring.

Tailor the level of due diligence

Controls are scaled according to risk:

- Standard due diligence for typical customers, combining identity verification with baseline financial information.

- Simplified due diligence (SDD) for low-risk situations (e.g., government pension funds or low-value accounts).

- Enhanced due diligence for higher-risk customers, such as PEPs or entities in jurisdictions with weak AML controls, involving deeper investigation and tighter controls.

For SDD, use OSINT to keep friction low. For EDD candidates, OSINT can justify escalation with evidence from public records, historic posts, and digital connections. Horizon® compiles that context into an auditable package without increasing the scope of data collection.

The initial ratings and risk factors established here flow directly into the enterprise-wide scoring and continuous risk updates described in Step 5.

Step 3: Beneficial ownership and KYB (Know Your Business)

Just as with customers, regulatory compliance for business entities goes beyond just verifying the legal name provided on the application form. KYB involves understanding the natural person(s) who ultimately own or control the business, known as the ultimate beneficial owners (UBOs).

Identify and verify UBOs

The institution must identify who directly or indirectly owns a significant stake (typically 25% or more) or who exercises effective control over the institution. Verification requires gathering personal ID documents for each UBO and validating with trusted sources.

Regulators treat ownership transparency as the heart of the standard:

“Transparency about who really owns and controls companies is essential to prevent them being misused for corrupt practices.”

– Xiangmin Liu, President of the FATF (2019–2020), Financial Times, November 2019.

Mapping those owners is exactly where OSINT adds value, connecting registries, filings and online footprints into a single ownership picture.

Map control structures and detect hidden arrangements

Opaque corporate structures, featuring layered subsidiaries, nominee directors, or shareholders, can be used to conceal beneficial ownership. Mapping the control hierarchy helps detect circular ownership structures, shell companies, or straw owners used for illicit purposes.

ShadowDragon’s tools visualize relationships between entities, domains, and key individuals, helping to reveal hidden control or coordination patterns that traditional registry checks might miss.

Use official registries and unique identifiers

Regulators and industry groups are increasingly recommending the use of official business registries and global unique identifiers, such as the Legal Entity Identifier (LEI), to validate company data and monitor cross-border relationships. Aggregating this information can enhance due diligence and create an auditable chain of ownership evidence. With ShadowDragon Horizon®, investigators can incorporate OSINT-driven insights that provide defensible context for beneficial ownership mapping, ensuring that business relationships are both transparent and verifiable across jurisdictions.

If organizations have transparent visibility into who ultimately owns and controls the businesses they transact with, they can greatly reduce the risk that their services will be used for money laundering, tax evasion, or sanctions evasion.

Step 4: Sanctions and watchlist screening

Having confirmed the identity and ownership of a customer, the institution must also verify that the customer or any associated party is not barred from doing business with the institution. Sanctions and watchlist screening involves checking customers and their relevant connections against restricted-party lists before onboarding and throughout the customer relationship.

Sanctions and watchlists

Customers, beneficial owners, and key counterparties are checked against major global and national sanctions lists, such as:

These lists identify individuals, companies, vessels, and jurisdictions subject to trade embargoes or financial restrictions. However, OSINT sources often reveal related entities, aliases, or infrastructure ties that sanctioned-party lists miss. Tools like ShadowDragon Horizon® surface these links across domains, emails, and networks to expose indirect risk relationships.

Politically exposed persons and adverse media

Sanctions screening typically also covers PEPs, including public officials and their family members and close associates, who may pose a higher corruption risk. It also includes an adverse media review to surface negative news, such as allegations of fraud, bribery, or organized crime, that may not appear on official sanctions lists.

The ability of ShadowDragon’s OSINT platform to aggregate open source data, public social media activity, and publicly available information augments this process, helping investigators evaluate credibility and context before escalation.

Continuous updates and automated tools

Sanctions lists and risk indicators can change daily. Financial institutions use automated, real-time systems to screen customers, beneficial owners, and even counterparty records against up-to-date watchlists and adverse media feeds.

These screening measures are a critical part of KYC checks. Robust systems incorporate fuzzy matching to minimize false positives and route matches that need manual evaluation to investigators. When escalations occur, ShadowDragon Horizon® preserves source data, timestamps, and investigative pivots, creating an auditable record of why a match was confirmed or dismissed.

Note: This step represents the initial and event-triggered screening. Continuous re-screening (the ongoing, periodic checks that detect new designations or changes in customer circumstances) occurs later as part of the ongoing monitoring process (Step 7).

Thorough and timely sanctions and watchlist screening at onboarding, combined with later re-screening, protects institutions from regulatory penalties and reputational damage while ensuring compliance with global AML obligations.

Step 5: Enterprise-level risk scoring

Institutions transition to this enterprise-level risk-scoring stage both after initial onboarding and continuously as customer activity occurs, moving beyond discrete due diligence decisions to capture and monitor data, which is then fed into dynamic, quantitative risk models for continuous, enterprise-wide risk management.

Data-driven modeling

Advanced analytics/machine-learning platforms ingest the CDD record, transaction history, sanctions-screening results, and adverse media hits. They output a composite risk score based on a variety of weighted factors, including transaction velocity, geographic exposure, counterparty behavior, and past trends of suspicious activity. Integrating OSINT insights into these models adds context beyond internal and regulatory data, capturing signals such as emerging reputational risks or illicit infrastructure uncovered through ShadowDragon Horizon®.

Dynamic rating updates

Unlike the initial CDD rating, this risk scoring is dynamic and ongoing. The ratings are updated as additional information becomes available. For example, a customer’s risk rating may be increased due to a surge in cross-border wire activity, a name/structure change, or a regulatory alert issued for a customer’s country of operation.

Institution-wide view

The aggregate results of this scoring are then fed into dashboards for senior compliance officers and regulators, as well as for capital allocation decisions, model validation exercises, enterprise risk appetite assessments, and other purposes. Automated triggers at this level can also trigger an automatic referral to EDD if the score breaches a threshold.

By transitioning from a static, customer-by-customer view to a continuous, data-driven enterprise-wide model, this step ensures risk management keeps pace with evolving behavior and regulatory expectations.

Step 6: Enhanced due diligence

Enhanced due diligence (EDD) is the deeper level of KYC verification applied to high-risk customers. EDD procedures are triggered when a customer is a politically exposed person (PEP), is based in a high-risk jurisdiction, has a complex or opaque ownership structure, or generates unusual or high-value transactions.

Under EDD, institutions collect source-of-funds and source-of-wealth evidence, screen adverse media, map beneficial ownership beyond the 25% threshold and apply more frequent ongoing monitoring. FATF Recommendation 10 requires firms to apply enhanced measures whenever money-laundering or terrorist-financing risk is higher.

In cases where a customer poses a higher risk based on geography, business sector, ownership, or politically exposed status, EDD may be conducted to provide greater assurance.

Gather further information

As part of an EDD process, institutions often require source-of-wealth and source-of-funds information to demonstrate how a customer accumulated assets and the origin of incoming funds. Audited financials, tax filings, and verified contracts for significant income streams may be used for this purpose.

OSINT sources can support these documents by surfacing additional details on asset ownership, undisclosed entities, and reputational risk exposure. ShadowDragon Horizon® consolidates this intelligence in a central platform, giving investigators evidence-based confidence before escalation.

Conduct more intensive ongoing monitoring

Ongoing monitoring of high-risk relationships typically requires more detailed scrutiny of transactions and shorter review cycles. Horizon® Monitor offers real-time OSINT monitoring to detect emerging red flags, such as social connections to sanctioned actors or sudden shifts in online behavior, before they appear in transaction records.

In addition to transaction monitoring, many institutions conduct real-time screening against sanctions lists, perform daily re-screening of customer data, and conduct thorough reviews of counterparties to identify unusual activity as it occurs.

Require senior management approval

Accounts subject to EDD are often required to be approved by senior management or the board. This is to ensure that senior management understands the risks associated with the relationship and that an enhanced level of oversight is in place to mitigate these risks.

Institutions use EDD measures where necessary to demonstrate to regulators that they are aware of and managing increased risk. By integrating ShadowDragon’s OSINT capabilities, compliance teams can document the rationale for escalation decisions using preserved source data and investigative trails, thereby strengthening auditability and regulatory compliance.

Step 7: Ongoing monitoring

KYC is not a one-time process; it requires continuous monitoring to ensure that customer behavior remains aligned with the risk profile established during onboarding and that new threats are identified in a timely manner.

Track transactions for unusual activity patterns

Financial institutions actively monitor transaction volume, frequency, and counterparties for any suspicious activity that could indicate money laundering or terrorist financing.

Red flags include unusual spikes in wire transfers, unexplained cash deposits, or transactions involving high-risk countries or territories. Automated transaction monitoring systems alert investigators when activity deviates from established baselines.

OSINT intelligence feeds can also be used to flag external risk signals (company registrations, activity associated with the customer, online communities reporting suspicious activity, etc.) that may indicate developing exposure. ShadowDragon Horizon® integrates these signals to strengthen early detection and alert context.

Perpetual or trigger-based KYC

Customer accounts are subject to periodic reviews based on risk ratings (e.g., annually for medium-risk customers) as well as trigger-based reviews when changes occur to the customer or its transactions. These reviews function as ongoing KYC monitoring, including regular KYC checks to ensure accuracy over time.

Changes could include a change of beneficial owner or control structure, or significant changes to transaction patterns or volume. This process, also known as perpetual KYC, is used to maintain up-to-date customer records, adjust risk ratings as needed, and support targeted KYC investigations.

Suspicious activity reports

If an investigation determines that customer activity is suspicious, institutions must report this information to the relevant regulator. This might be the Financial Crimes Enforcement Network (FinCEN) in the US, the Financial Intelligence Unit (FIU) in the EU, or a similar national regulator.

These Suspicious Activity Reports (SARs) are filed within the prescribed time limit to avoid regulatory fines and support law enforcement. ShadowDragon Horizon® preserves every data source, timestamp, and investigative path, giving analysts the defensible audit trail regulators expect.

Closing the KYC loop involves ongoing activities that keep customer information up to date, detect changes in risk profiles in real time, and file SARs as necessary to comply with AML regulations worldwide.

Step 8: Recordkeeping and reporting

The final step in a complete KYC program is rigorous recordkeeping and reporting. This preserves an auditable trail of every decision, supporting both internal governance and regulatory oversight.

Retain KYC documentation

Financial institutions are required to retain records of customer identification information, due diligence files, risk assessment results, and transaction histories for a period specified by applicable laws and regulations, typically ranging from five to seven years after the account is closed or the transaction is completed.

This information should be stored securely, in accordance with data protection standards, and in a manner that allows for easy retrieval when necessary. It can be stored on-site or, if managed with adequate controls, in a compliant cloud-based system.

Prepare for audits and ensure traceability

Audits may take place at any time, and regulators will want to know not only what decisions were made but also why and how. This is why KYC recordkeeping and reporting are so important.

Auditors must be able to follow the verification, ownership, monitoring, and escalation steps without any gaps in traceability. Each decision and action taken should be adequately recorded, accompanied by explanations and, where appropriate, supporting evidence. ShadowDragon provides traceability by capturing each investigative step, allowing reviewers to reconstruct decision logic with full transparency.

Integrate with AML monitoring and reporting

KYC information also needs to integrate with and support the ongoing transaction monitoring system used for AML reporting. This will ensure timely and accurate detection of suspicious activity and the creation and submission of SARs or similar regulatory filings. KYC information can also support periodic regulatory reporting, such as beneficial ownership reporting.

Effective recordkeeping and reporting not only help to ensure compliance with reporting obligations but also enable quicker response to investigations.

Integrating OSINT data from ShadowDragon Horizon® ensures that all intelligence used in decision-making is properly documented, defensible, and available for regulator review, closing the KYC loop with transparency and accountability.

Nico Dekens – aka “Dutch OSINT Guy”

Nico Dekens – aka “Dutch OSINT Guy”